Good morning, and welcome to TEG Transport Insights.

For much of our sector’s history, transport managers have favoured small carrier networks. In logistics, margins for error are slight. Keeping networks small grants managers both reliability and control, reducing the potential for delivery issues.

Recently, however, the drawbacks of the small-network model have become harder to justify. RHA figures suggest that, since 2019, the costs of running an artic have increased by almost 40%1. Over the same period, the price of artic capacity has increased by just 15%2. With margins under siege, 3PLs are axing operational inefficiencies. And small carrier networks are rarely efficient.

The enticing economics of large carrier networks

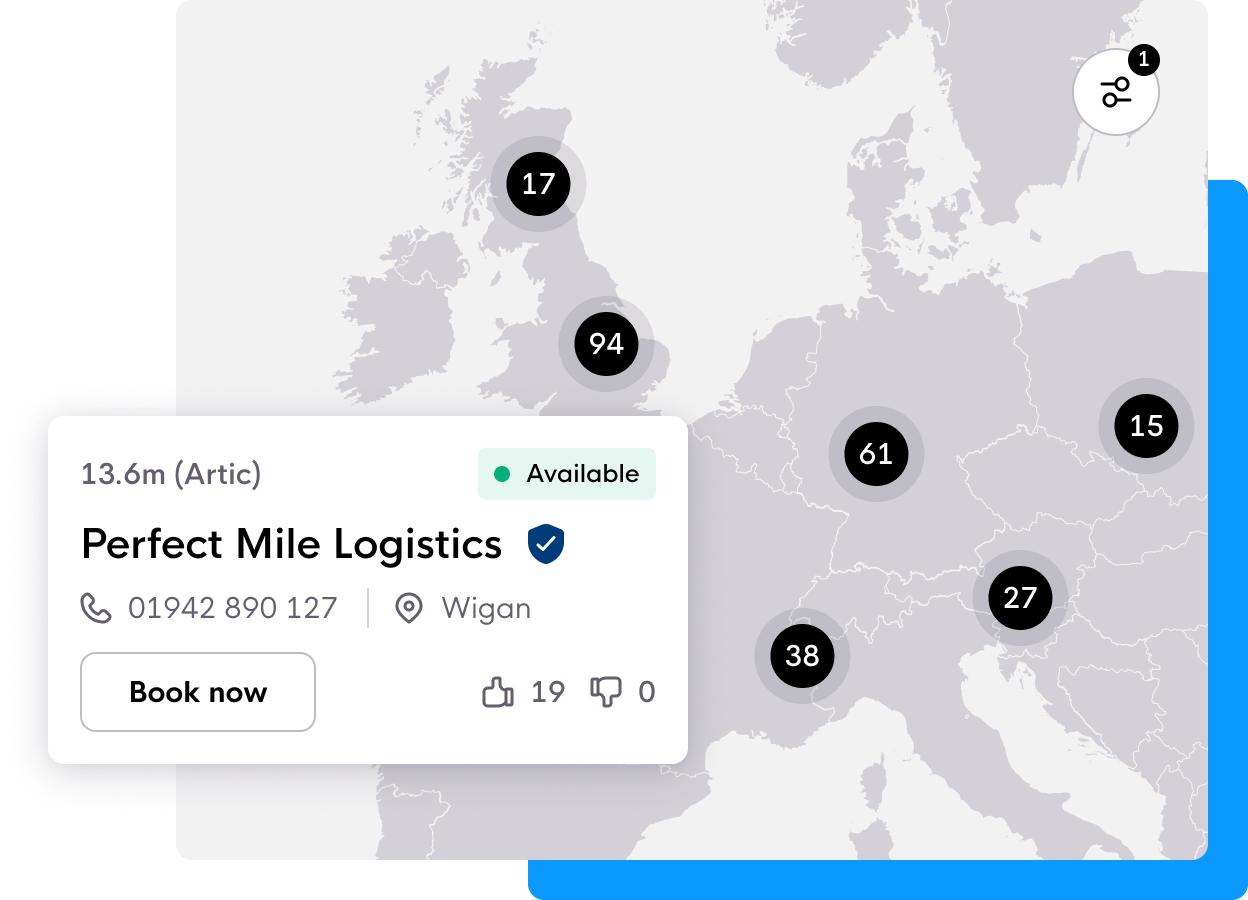

Make no mistake, transport teams who work with relatively small carrier networks will almost always find an appropriate carrier for a contract. But transport teams who work with large carrier networks can find optimal carriers, whose rates are entirely market-defined. Those with large carrier networks pay no premium to cover a few more empty miles. The market scrubs costly empty miles out.

Carrier networks have grown by 58%

The opportunity for gains, it would seem, has not gone unnoticed. While the proprietary nature of network size makes it hard to pinpoint precise growth statistics, TEG data offers a clue. Every year since 2020, the average size of a typical TEG member’s carrier network has increased. Indeed, in 2025, carrier networks are a full 58% broader than their 2020 equivalents. Elsewhere, 3PLs increasingly promote their services not by listing asset inventories but instead by talking of access to vast, efficient carrier ecosystems spanning dozens of countries. Even where precise carrier counts go undisclosed, the emphasis has clearly shifted.

Why now?

Of course, in logistics, leaders continually seek efficiency gains. If broadening carrier networks made for leaner operations, would transport teams not have made the switch long ago?

Probably not. Historically, transport teams have managed their carriers through a combination of address books and phone calls, capping network size. Leaning on personal relationships to safeguard carrier performance further limited scale.

Today, digital technologies eliminate network limits. Tech like TEG’s partner Trustd, for example, allows 3PLs to monitor carrier compliance at scale and in real-time, while supplementary software can monitor carrier performance over time. Tracking technologies can grant managers 360° carrier control towers, no matter how much freight they have in motion. Advanced options highlight delivery risks.

Choice for 3PLs. Choice for carriers.

None of this is to say that strong relationships between transport teams and their carriers are becoming less important. A large carrier network remains large only when its carriers remain happy.

What is becoming more important is choice – on both sides of the bargain. Just as 3PLs must protect margins, so must carriers. By working together more efficiently, both parties benefit.

Large carrier networks are therefore unlikely to be experimental. Thanks to technological progress, they’re becoming inevitable.

James Mead

TEG Head of Enterprise