TEG Index at a glance

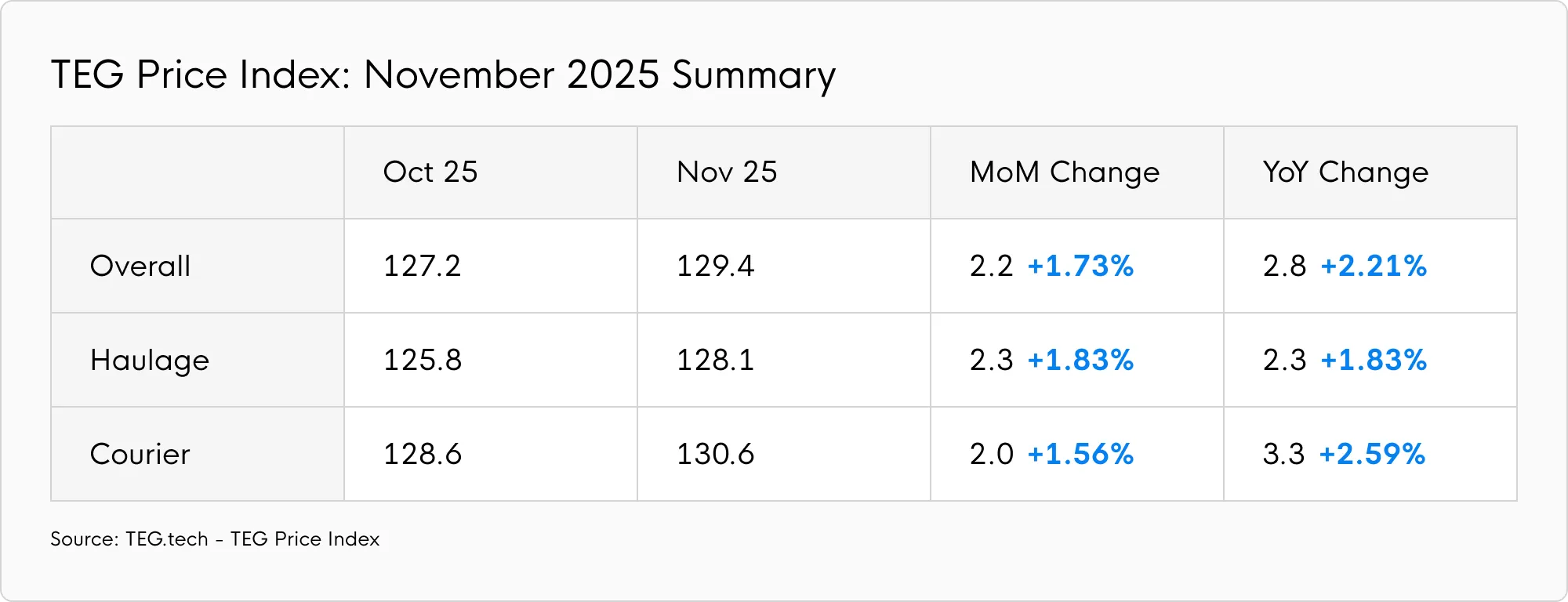

The TEG Price Index rose 2.2 points (1.73%) to 129.4 in November. There has never been such a substantial November rise since the index launched in 2019.

The Haulage Index was equally buoyant last month. It rose 2.3 points (1.83%) to reach 128.1. Year-on-year, the haulage increase was identical – 2.3 points and 1.83%. Looking specifically at artic vehicles, the November increase was 2.2 points (1.9%), mirroring overall haulage growth.

As for the Courier Index, it rose by 2 points (1.56%) last month to reach 130.6, resulting in a slightly stronger 3.3-point (2.59%) annual rise.

About turn for carrier availability

Having experienced two months of robust growth in carrier availability – including a 21.7% increase in October alone – November saw a significant 22.4% carrier availability fall, creating the tightest market conditions in months.

Meanwhile, overall transport demand continued to increase (and for specific vehicle types) suggesting a push ahead of Black Friday as companies moved large goods to distribution centres.

Overall carrier demand rose 4.79% in November, while demand for artic vehicles increased 8.32%. As a whole, haulage demand rose 2.62%.

At a time when the RHA reports that around 100,000 HGV drivers have allowed their Driver Qualification Card (DQC) to lapse in the last year, and when average HGV salaries are up 9.26%, November’s TEG Index suggests 3PLs are leveraging more and more third-party partnerships to fulfil increasing demand.

Has the late Black Friday helped with growth?

DHL’s eCommerce Trends Report recently revealed 84% of online retailers were banking on a sales surge in November. Meanwhile PwC predicted Black Friday spending would reach £6.4bn in 2025, 1.5% higher than last year.

It’s too early to know whether those precise predictions have materialised, but despite continued budget apprehension throughout November and measures announcing cost of living hikes for most people, Black Friday purchases were alive and well.

Early TEG data shows healthy transport demand. Elsewhere, Nationwide Building Society published live data throughout Friday 28 November and, by 4pm, its customers had made 7.3 million transactions since the beginning of Black Friday – a 9.18% jump vs Black Friday 2024.

What we’re yet to understand is the total value of consumer transactions. But even if people have bought lower value items, the volume looks to have been there for transport providers. If history is to be trusted, our sector should expect a busy December.

Industry pulse

The economy continued to run hot during November with inflation sticking at 3.6%. The Office for Budget Responsibility (OBR) has revised its forecasts, suggesting the annual inflation rate will be 3.5% with 2026 settling to 2.5%. Meanwhile, the Bank of England held the interest rate at 4% in November, with some predicting an upcoming cut on 18 December.

Ahead of the budget, the GfK Consumer Confidence Index dropped 2% and business predictions, not surprisingly, remained mixed. For example, the ONS Business Insights and Conditions Survey reported on the two weeks ending 16 November and showed 18.8% of respondents thought their business’s performance would increase over the next 12 months – while 16.1% thought it would decrease.

This scenario does suggest that a consumer ‘vibecession’ – a disconnect between negative consumer sentiment and a relatively stable economy – may be unfolding once again.

It’s too early to understand what impact the November budget will have on consumer and business confidence. Most consumers will see an impact on their disposable income and businesses will need to prepare for several changes, such as a rise in the National Living Wage from April 2026. For the next month, at least, we can expect to see typically strong transport prices as festive demand peaks.

Fuel Watch

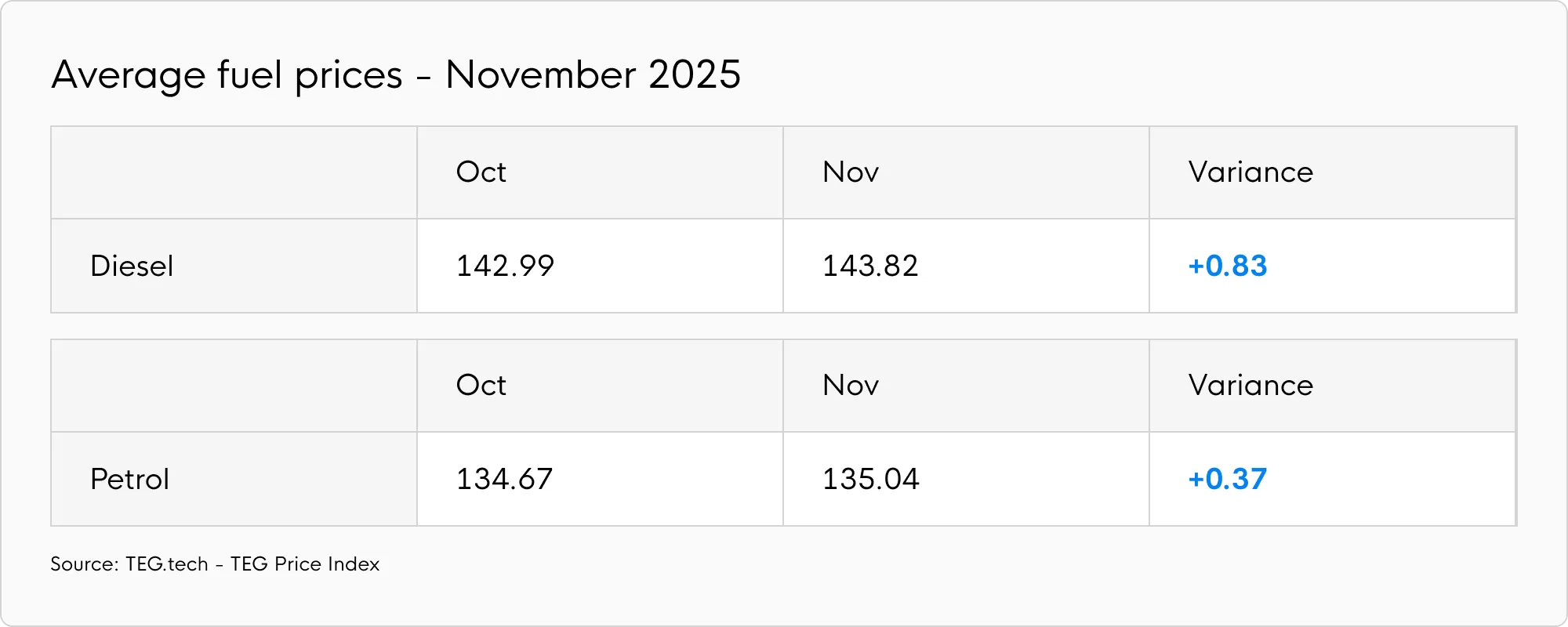

Fuel prices increased in November, with rates rising from week commencing 24 November – especially for diesel.

Average diesel prices rose to 143.82p per litre in November, an increase of 0.83p (0.58%). Year-on-year, the rise was 3.35p per litre (2.38%).

The monthly petrol increase was more muted with the average price per litre increasing to 135.04p, just 0.37p per litre (0.27%).

While it’s a relief to hear the government will now freeze fuel duty until September 2026, the benefit will subsequently end after a 15-year period, placing upwards pressure on prices. Of course, there’s still scope for Chancellor Rachel Reeves to change this in the spring budget.

Expert comment

“When things do pick up, either for Xmas peak or beyond, make sure you’re ready. It’s an obvious thing to say, but the budget being so close to a late Black Friday has meant that this is yet another unusual year. The press hasn’t helped by being so down about everyone’s finances – the ghost of direct debits yet to come! There probably is a driver shortage, but it may not be overly apparent because of the state of the economy.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd

The TEG Price Index helps freight buyers stay ahead of change. Use it alongside our Analytics and Insights module to make strategic, data-driven logistics decisions.