TEG Index at a glance

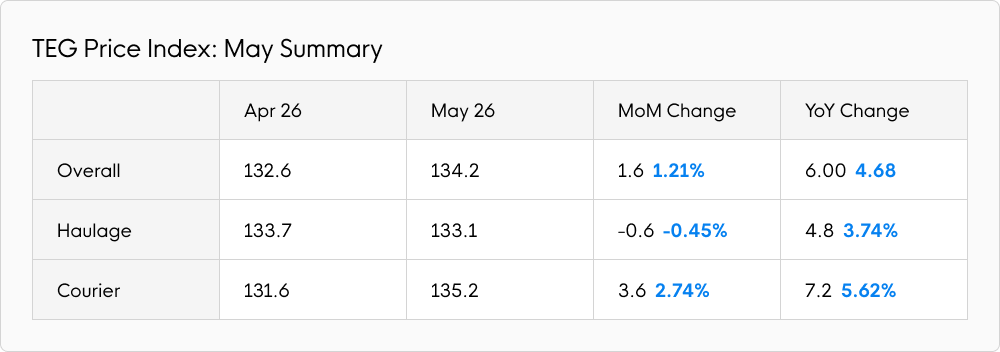

The TEG Price Index rose by 1.6 points (1.21%) in May to reach 134.2. After a 7.8-point price rise in April, last month appeared to be steadier for transport operators. But the modest increase was inconsistent between the Courier and Haulage Indexes.

In contrast to an overall 1.6-point rise, the Haulage Index fell by 0.6 points (0.45%) to reach 133.1. Artic pricing followed the trend, falling 0.5 points (0.4%) to 125.2. Meanwhile, the Courier Index rose by 3.6 points (2.74%) to reach 135.2.

This index divergence, albeit slight, correlates with demand patterns atypical of May, a month in which haulage demand fell unexpectedly. It’s too early to tell whether the change is significant, so the coming months will provide more meaningful data.

Year-on-year, the situation was more in line with expectations. The overall TEG Index rose by 6 points (4.68%) while Courier and Haulage followed suit, growing by 5.62% and 3.74% respectively.

Has lower confidence in major purchases suppressed demand?

For the last two years, overall transport demand has grown in May: 10.30% in 2025 and 21.19% in 2024. Last month, demand rose by just 2.21%. Given the two bank holiday weekends and a late spell of warmer weather, larger growth may well have been expected.

Haulage demand, in particular, hampered the overall demand increase – last month, demand for haulage vehicles fell by 2.84%. Given the GfK Major Purchase Index dropped two points in May, consumers may have begun to delay larger purchases that typically require haulage logistics. Elsewhere, reports of a shrinking UK manufacturing sector could also play an explanatory role.

Demand aside, transport availability fell by 10.29% in May. The contraction is typical of seasonal patterns, as the industry accommodates bank holiday leave. Interestingly, haulage availability was almost level, once again failing to align with aggregate patterns.

Fuel watch

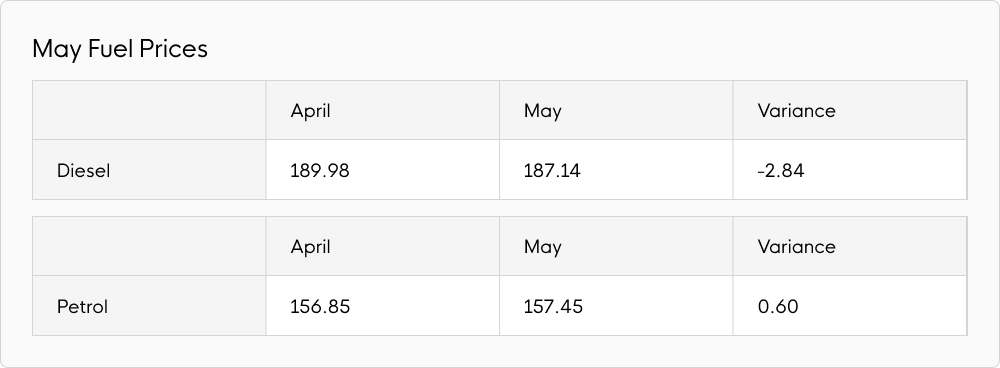

May saw fuel prices ease following significant growth during April. While welcome news, this may only be a temporary reprieve.

The big news concerned a 2.84p (1.49%) fall in average diesel prices to 187.14p per litre. Diesel is now 48.09p per litre (34.58%) higher than 12 months ago.

Average petrol prices rose just 0.60p (0.38%) to reach 157.45p per litre. In May 2025, the price was 25.06p per litre (18.93%) lower.

As the Strait of Hormuz remains effectively closed and activity once again escalates between the US and Iran, experts predict we should anticipate high fuel prices for many months to come.

Moves to support high fuel prices

To bolster global oil supplies, the International Energy Agency has been coordinating collective government action to release reserves into the market. With Brent crude trading 4% lower than a week earlier (22 May) and diesel prices easing, the effort appears to be helping.

According to the IEA, cumulative oil production losses since February have now reached 12.8 million barrels a day. As of 8 May, 164 million barrels of oil have been released under the 400-million-barrel commitment. However, rebuilding stocks could take up to three years on current predictions.

Domestically, the country welcomed UK fuel price relief as the government announced an extension to the temporary 5p duty cut until the end of 2026. Helping millions of households that run cars, the move will also support businesses across all sectors. In addition, the government introduced specific support for hauliers last month: a 12-month road tax holiday (starting 1 July 2026), with qualifying vehicles paying just £1 on renewal, plus the HGV levy. A typical heavy goods lorry could save up to £600, with the largest vehicles saving as much as £912.

Industry pulse

While some UK economic indicators surprised analysts last month, there’s no doubt the forecast looks challenging for the rest of the year. With the cost of living in sharp focus for the government, it recently announced a collection of summertime measures to ease certain costs for households.

Inflation fell to 2.8% in the year to April. Down from 3.3% in March, this wasn’t expected. With lower energy prices contributing to the situation, experts still expect the rate to be near 4% by the end of the year. Interest rates remain on hold at 3.75%.

The GfK Consumer Confidence Index rose two points overall in May. Surprisingly, confidence in the General Economic Situation for the Next 12 Months rose by five points. And yet, the Major Purchase Index fell by two points. This suggests that while consumers may have felt a little more confident last month as the spring season developed, the sentiment is likely to be short-lived. And there appears insufficient consumer confidence to make larger purchases in the coming months, especially in lower income households.

Recently released unemployment figures show rates have risen to 5% in three months to March, compared to 4.9% in three months to February. Vacancies dropped by 3.9% between February and April, suggesting companies may be pausing recruitment during uncertainty. They might also be feeling the impact of higher labour costs following April changes to employment taxes.

Energy regulator Ofgem announced a 13% increase of the price cap from 1 July until 30 September. While widely anticipated, this is likely to be a blow to the UK economy in the months ahead as the typical household feels the £221-a-year increase. It will also affect operating costs for businesses.

Expert comment

“What an interesting month May has been, with a record-breaking heatwave, local elections and all the political shenanigans around the forthcoming Makerfield by-election. But the TEG Haulage index for May is showing very little change against April. Unsurprising, since diesel prices are drifting down, although still above where they were at this point after the Ukraine invasion, HGV traffic levels mid-April returned to ‘normal’ after having been low in earlier in the year and HGV wages in job ads apparently pretty flat.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd