TEG Index at a glance

Despite talk of upcoming oil shortages in Europe, fuel price increases seem yet to have impacted transport rates.

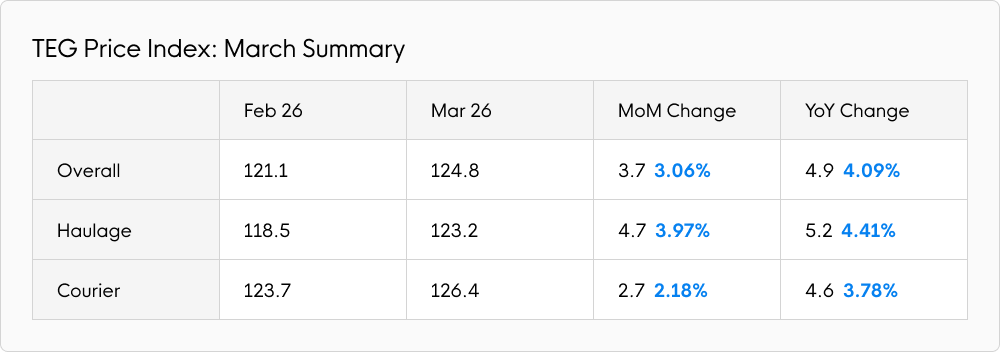

The TEG Price Index increased by 3.7 points (3.06%) in March to reach 124.8, an increase almost entirely attributable to heightened Easter demand. Year-on-year, transport prices increased by 4.9 points (4.09%), an increase once again reflected by the impact of Easter.

The Haulage Index saw the biggest month-on-month rise, increasing 4.7 points (3.97%) to 123.2. Year-on-year, growth was 5.2 points (4.41%). This was influenced by strong growth in the Artic Index, a busy segment within haulage. It rose 5.3 points (4.8%) to 114.7 in March. Compared to March 2025, the Artic Index was 3.4 points (3.05%) higher.

Meanwhile, the Courier Index moved up by 2.7 points (2.18%) in March to reach 126.4. Year-on-year, it grew by 4.6 points (3.78%).

With Easter falling earlier than in 2025, it was no surprise to see transport prices rising across the board last month. That increased oil prices are yet to impact transport rates is, however, unexpected.

Fuel watch

The media has widely reported fuel prices rising during March. The conflict in Iran quickly influenced oil prices and it’s likely we’ll see further activity during April.

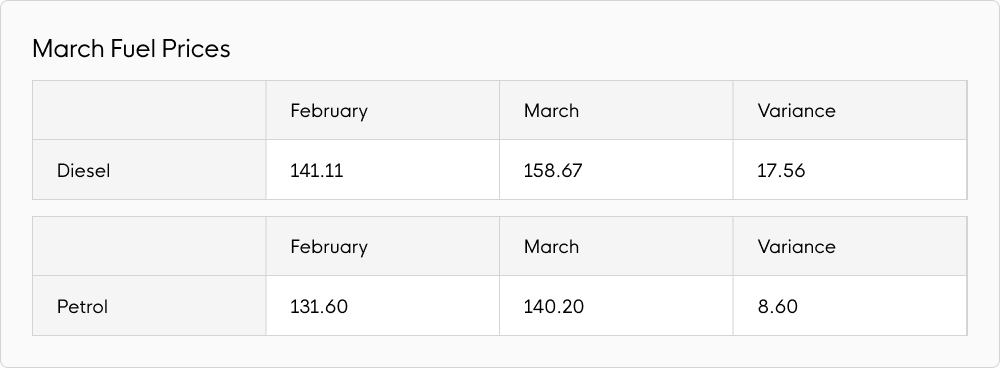

The average petrol price rose by 8.6p per litre (6.53%) last month, to reach 140.2p. Compared to March 2025, the price of petrol was 2.7p per litre (1.96%) higher.

As for diesel, the average price rose by 17.56p per litre (12.44%) in March to 158.67p, which was 13.84p per litre (9.56%) higher than in March 2025.

The picture was a little bleaker when singling out average fuel price rises last week (ending 30 March). Petrol stood at 148.78p per litre and diesel was 176.52p per litre. We may not have reached the top of the curve just yet.

The fuel price challenge

In transport, when fuel prices increase, someone, somewhere pays the price.

Last month, carriers without built-in fuel escalators appeared to absorb higher fuel prices at the pumps, adopting a “wait-and-see” approach. But this won’t be sustainable given how tight transport operator margins are, especially as many suggest higher fuel prices may be here to stay.

By contrast, those with fuel price escalators on contract work will feel protected in the short term. But the picture could become more complex if the Middle East conflict continues for some time. For example, instead of accepting higher transport prices, shippers could move away from road logistics, transport more goods less frequently, or source more locally.

Whatever happens next, fuel prices are set to reflect the relative price of Brent crude oil, which is currently around 50% higher than before the conflict in Iran started. At present, oil prices fluctuate in line with the sentiments of US President Donald Trump. At the time of writing, Mr. Trump had suggested the Iran war may cease in “two to three weeks”, however such sentiment often reverts.

Easter demand increases rates

Despite global events, March rates were somewhat “business as usual” for the sector.

Easter’s transport activity took place almost entirely in March this year, prompting transport demand to increase by 19.6% month-on-month. Meanwhile, availability fell by 7.2% across the market in March, reflecting the additional demand placed on a fixed number of vehicles.

The predictable combination of augmented demand and reduced supply increased transport rates.

Industry pulse

Uncertain on how the Iran conflict will affect the UK economy in the months ahead, the Bank of England voted to hold interest rates at 3.75% in March. They’ll be waiting to see what happens to inflation, which is predicted to rise from the 3% reported in February. We’ll find out on 22 April. Experts predict that UK interest rates could rise as soon as next month in a bid to curb fresh inflation.

Meanwhile, the Institute of Grocery Distribution (IGD) has suggested that food inflation could reach 6.4% across 2026, mainly due to increased costs of fertilizer and fuel.

As a result of global events, the Organisation of Economic Co-operation and Development (OECD) has recently downgraded its economic growth prediction for the UK to 0.7% (down from 1.2%) and also expects higher inflation in the coming months.

It was not surprising, then, that the GfK Consumer Confidence Index dropped two points in March. More noteworthy, the score for “General economic situation over the next 12 months” dropped six points and the Major Purchase Index fell by four points in March. Consumers appear to be bracing themselves, and Neil Bellamy, Consumer Insights Director at GfK described the situation as a “ripple of fear”.

Changes to legislation from April 2026 will present transport operators with several labour cost increases to absorb, such as a rise in the legal minimum wage to £12.71 per hour and the implementation of the Employment Rights Act 2025. This includes broadening statutory sick pay coverage and offering paternity leave rights from day one of employment.

In a positive move for the transport sector, the government announced a £1 billion investment in electric HGVs and infrastructure last week. This will give hauliers up to £81,000 off zero emission trucks and £5,000 discounts off e-vans. The government also added another £170 million to its existing charging scheme.

Designed to support two of the biggest hurdles to electrification – upfront costs and access to charging – some in the industry have said you can’t just “throw money” at the problem. But given global fuel price uncertainty, the move may help some transport operators transition towards a more sustainable fuel source.

Expert comment

“Anything I say about diesel prices will be out of date by the time you read this… however quick you are! What can be said is that pump prices are going up further than the increase caused by the invasion of Ukraine. And that hauliers buying diesel in bulk, or on some fuel cards, seem more quickly exposed to increases than the general public.

“Just when the Governor of the Bank of England must have been thinking: ‘Phew!, I don’t need to write yet another letter to the Chancellor to explain why I’ve not met my KPI’, increased inflation looks inevitable.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd