TEG Index at a glance

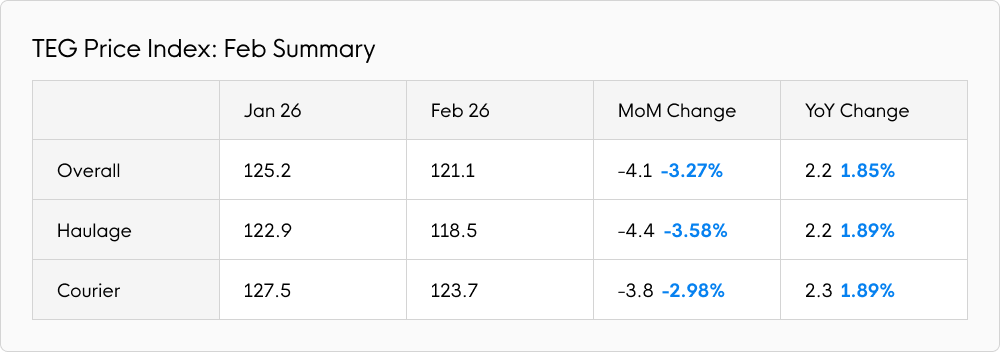

Following a significant transport price drop in January, the TEG Price Index fell by a further 4.1 points (3.27%) during February to 121.1. This follows the usual trend seen at this time of year. Compared to February 2025, the index rose by 2.2 points (1.85%).

Transport price reductions were evident for both haulage and courier services in February. The Haulage Index dropped by 4.4 points (3.58%) to 118.5, still remaining 2.2 points (1.89%) higher than in February 2025. Meanwhile, the Courier Index fell by 3.8 points (2.98%) to 123.7. Compared to 12 months ago, it was 2.3 points (1.89%) higher.

The Artic Index dropped a little further. It fell by 5.3 points (4.6%) to reach 109.4. In February 2025, Artic stood at 109.5, 0.1 points (0.09%) higher than its current position.

Given low demand for transportation after the festive season, it’s common to experience lower prices ahead of spring.

High availability dampens prices

While month-on-month demand for transport remained almost level in February, availability rose by 10.7% compared to January 2026. With ample capacity in the system, transport prices fell.

February is typically a quiet time for transportation as consumers rein in their spending after the Christmas season, leaving fewer goods to transport.

March usually sees that situation change as the spring season looms and signs of warmer weather boost spirits. But this year, all eyes will be on the conflict in the Middle East and the extent to which it impacts the global economy.

A “dull” month for confidence

The GfK Consumer Confidence Index fell by three points in February. While recent months have seen indications of increased optimism, gloomy weather may have contributed to weaker perceptions of personal finances, with fewer people inclined to make major purchases.

“Although the rate of inflation is easing, prices continue to rise, forcing many households to prioritise day-to-day spending over longer-term needs,” said Neil Bellamy, Consumer Insights Director at GfK.

The Met Office confirmed that, weather-wise, February was the UK’s fourth dullest on record and 23% wetter than average (rising to 70% wetter than average when looking at just England). Thankfully, March looks more promising.

The latest ONS Business Insights and Conditions Survey suggests businesses saw through early February rain clouds, at least. In the two weeks ending 15 February 2026, 23.2% of respondents thought their business’s performance would increase over the next 12 months, while only 14.0% thought it would decrease.

Industry pulse

The welcome drop in inflation to 3% (down from 3.4% in December) reported on 18 February was apparently driven by lower food and fuel prices. The ONS reported the drop one week after the Bank of England held interest rates at 3.75% on 5 February.

Elsewhere, average HGV salary dropped 0.78% month-on-month in February to £41,079, aligning with an increase in driver vacancies. At the same time, Adzuna reported the national average salary jumped by 2.27% month-on-month in February, to £43,273.

According to a recent report from accounting and business advisory firm BDO LLP, there was a 26% drop in logistics merger and acquisition (M&A) deals during 2025 compared to 2024. Last year saw 69 completed deals whereas 2024 recorded 93. This, said BDO, is down to economic and geopolitical uncertainty.

The situation in the Middle East led geopolitical concerns in February and continues to gather pace as we enter March. The biggest risk to transportation is an ongoing elevation in oil prices attributable to tumult in the Strait of Hormuz, through which 20% of the world’s oil and gas usually travels. Following air strikes on Iran, crude oil prices have already jumped by 10%. The world now hopes the conflict is brief.

Back home in the UK, spring sunshine has finally arrived. With it comes the potential uplift from events such as Mother’s Day and the Easter long weekend (2-5 April). Let’s hope this typically busy time of year for transport isn’t impacted by events abroad.

Are fuel price rises inevitable?

Given the Middle Eastern conflict, which is currently unfolding by the day, it’s worth considering what may happen to fuel prices in the coming weeks and months.

History tells us that oil supply disruption, however short term, generally increases fuel prices. We also know that fuel prices are quick to rise and slow to fall. The risk of geopolitical events, especially in the Middle East, is that they impact oil supply and global logistics, with no certainty of the outcome or timeframe.

Europe is, therefore, bracing for a fuel cost rise that could affect prices, in the short term and for months to come. In the UK, the AA has already suggested we might see fuel prices return to where they were at the start of the year in a matter of weeks. Increased fuel costs would likely throw inflation off its current, downward trajectory, which could even trigger interest rate increases.

Clarity remains elusive, but the uncertain global situation does demonstrate the critical need for 3PLs to embed agility into their operations so they can quickly and cost-effectively react to shifts in demand. Solutions such as TEG Carrier Sourcing can help.

Fuel Watch

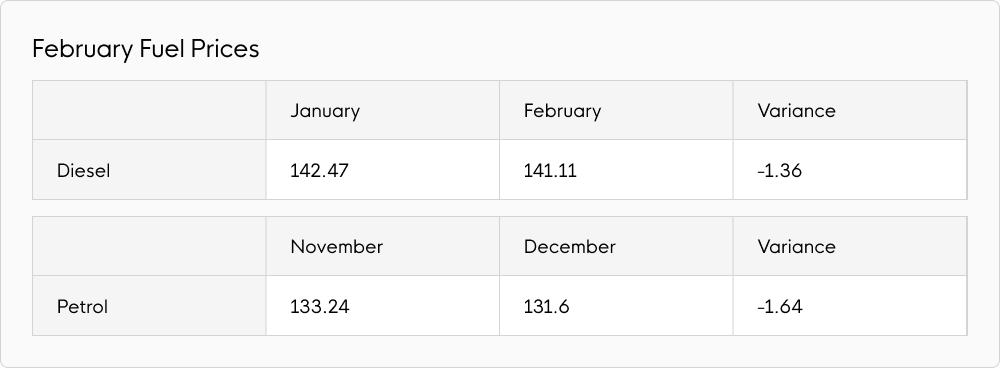

While international events may drive up fuel prices in the coming months, February saw both petrol and diesel prices fall.

At an average of 131.60p per litre, petrol prices fell by 1.64p (1.23%). Compared to February 2025, the average petrol price was 7.55p per litre (5.43%) lower last month.

Average diesel prices also fell again in February, reaching 141.11p per litre. This was a 1.36p (0.95%) month-on-month drop and a 5.31p (3.63%) year-on-year reduction.

Expert comment

“February would surely be the shippers’ favourite time of year, with haulage rates at their lowest in the calendar year… if they had many goods to ship! The nature of supply and demand means that unless they have completely counter-cyclical trade patterns (think garden furniture) there’s no advantage.

Then, as we go further into Spring, retail starts to pick up as Mother’s Day, and then Easter (in the first week of April this year), mean that we all come out of hibernation and start spending again. And then, ‘sure as eggs is eggs’, haulage volumes and rates will start to go up again, to the relief of the provider.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd