TEG Index at a glance

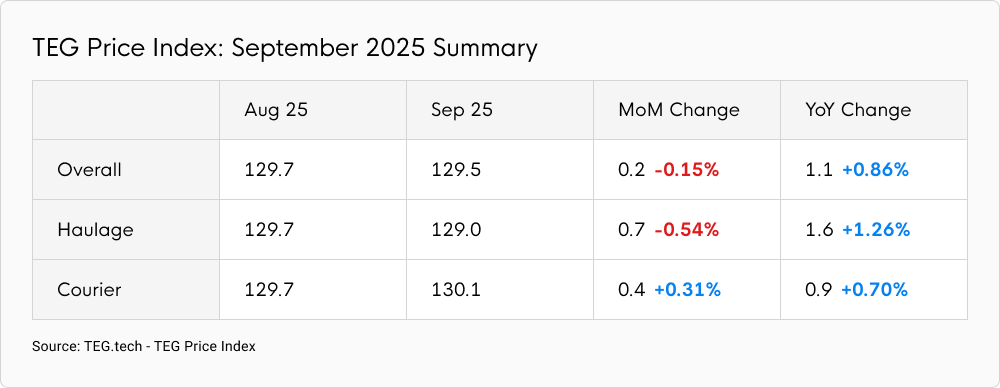

The TEG Price Index fell 0.2 points (0.15%) in September to reach 129.5. The Index hasn’t seen a September drop since its inception in 2019.

Reflecting the off-trend move, the Haulage Index fell by 0.7 points (0.54%) in September to 129.0. It now stands 1.6 points (1.26%) higher than in September 2024.

The Courier Index, however, rose 0.4 points (0.31%) to 130.1, putting it 0.9 points (0.70%) higher than 12 months ago.

Adding further insight, the price index for artic vehicles dropped 1.6 points (1.3%) in September to 120.1. This contrasted significantly with past September trends; in 2024 it jumped 0.8 points and in 2023 it rose 2.5 points.

Availability jumps while demand drops

Artic availability soared by 37% in September. In contrast, artic demand dropped by 10% following the August high, which was bolstered by an unusually warm and sunny bank holiday weekend.

Heightened availability and declining demand clearly altered the course of transport pricing during September this year – a month when we typically see a notable rise in prices as autumn begins. The demand drop may be partly explained by reduced business and consumer confidence (see ‘Industry Pulse’ below). Meanwhile, a fall in fuel prices likely also affected rates.

So far, the 2025 TEG Price Index has proved less predictable than in years gone by, reinforcing the need to remain data-informed when making pricing decisions.

The HGV driver conundrum

Last month, we reported on the apparent UK HGV driver shortage, with Adzuna data showing 4,027 vacancies in August. Vacancies rose to 4,212 in September, and the average driver salary increased by 0.71%, up to £42,422.

Given the 36% jump in artic availability we saw in September, the situation is perhaps more complex than vacancy statistics intimate. In particular, reports – and now data – suggest HGV drivers may be changing how they work, favouring agency work over contractual employment and working more in months they wish to earn. It could be that many drivers chose to work less during the warm, summer months, and are now returning to the workplace as peak season approaches. This logic would certainly explain the high level of artic availability that muted September 2025 rates.

Industry pulse

The economic mood was somewhat cautious in September. The Bank of England held interest rates at 4% following a 0.25% drop in August. It also predicted inflation would rise further during September, from 3.8% to 4.0%. We await official figures.

According to the Institute of Directors Economic Confidence Index, business confidence fell to a new record low in September. Measuring business leader optimism in prospects for the UK economy, the index dropped to -74 in September, down from -61 in August.

The GfK Consumer Confidence Index also fell in September, by two points, negating the optimism reported in August. As Chancellor of the Exchequer, Rachel Reeves, hints at further tax rises and “hard choices” in November’s Budget, perhaps consumer apprehension has hit short-term spending.

September also demonstrated how a sizeable supply chain can be toppled overnight without warning. Jaguar Land Rover’s cyberattack reportedly upset supplies from around 700 UK companies that contribute to making the estimated 30,000 parts each luxury car requires.

On a more positive note, industry peak season is fast approaching, and increased transport demand is expected as we close in on events like Black Friday and the traditional festive season.

Fuel Watch

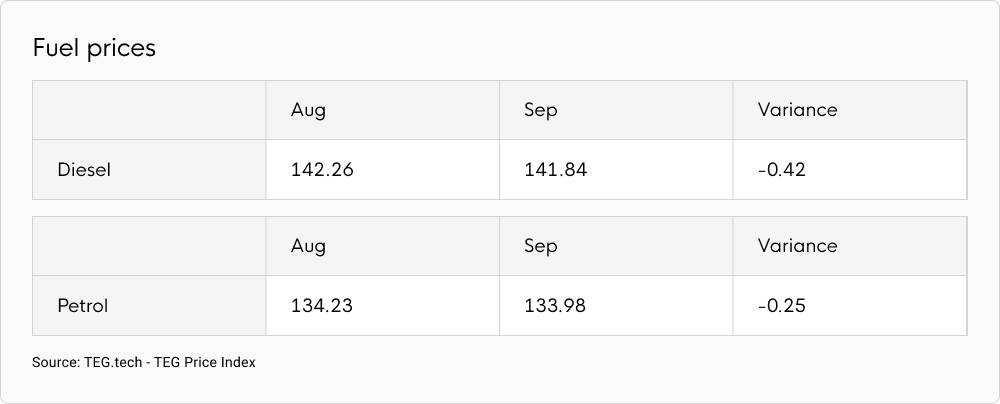

In line with speculation, fuel prices dropped in September.

Diesel prices averaged 141.84p per litre during September. At 0.42p per litre (0.30%) lower than August, the drop was muted. Interestingly, the September diesel price was just 0.03p per litre (0.02%) higher than 12 months ago.

Average petrol prices in September also fell. They dropped by 0.25p per litre (0.19%) to 133.98p per litre. Compared with September 2024, that’s 2.81p per litre (2.05%) lower.

In the latest Competition and Markets Authority monitoring report, the CMA said it was worried fuel margins remained higher than historical averages and continued to creep upwards. It found that supermarket retailers’ margins were 4% in 2017 but averaged 8.4% across the first half of this year. Non-supermarket retailer fuel margins were 6.4% in 2017 but averaged 9.8% in the first half of 2025.

Expert comment

“OK, so I was wrong a month or so ago when I thought that life was back to normal! I don’t know how many freight movements go in and out of JLR and between its various suppliers, but I’m wondering about the extent of the impact to the hundreds of companies that won’t have been making deliveries during September. Any haulier normally involved in those movements will have been looking for work elsewhere, which may explain the TEG Haulage Index not having the uplift one might have expected.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd

Have you registered for our webinar?

Hear from TEG’s James Mead and Aricia Ltd’s Kirsten Tisdale in our 30-minute pricing webinar on 8 October: Bucking the trend: How to use data, not precedent, to price during peak.

Together, they’ll show how past trends can be misleading and why using market data to price during peak can minimise chaos and maximise outcomes.