TEG Index at a glance

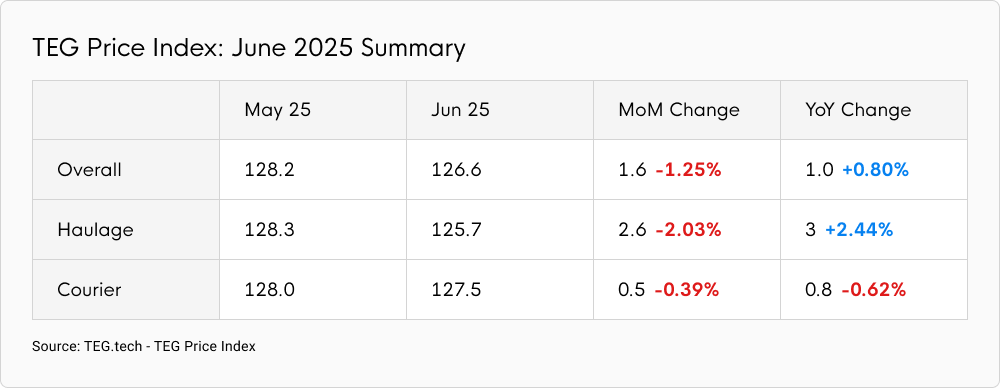

Bucking the typical summer trend, the TEG Price Index fell 1.6 points (1.25%) last month to 126.6. Compared to a year ago, the June 2025 Index was 1.0 point (0.80%) higher.

The Haulage Price Index fell 2.6 points (2.03%) in June to 125.7. The significant reduction was mirrored by the ‘Artic Index’, which fell 2.2 points (1.83%) simultaneously. Year-on-year, the Haulage Index was up 3 points (2.44%).

Movement in the Courier Index was less marked: it fell 0.5 points (0.39%) in June to 127.5. This was 0.8 points (0.62%) lower than June 2024.

A sharp and unexpected fall

A drop in the TEG Price Index during June was not expected. The Index has increased throughout June for the past five years straight, usually owing to the busy summer season gaining momentum. The surprise reduction reinforces the industry’s current mantra. After years of uncertainty, in 2025, we must expect the unexpected.

Delving deeper, TEG data show haulage demand plummeted by 13.04% in June, while supply of haulage vehicles – and artics – increased. Little wonder, then, that prices fell.

While a transport price reduction was unexpected given historical trends, the reduction aligns with anecdotal industry sentiment. In recent conversations, TEG partners have bemoaned idle capacity. Asset-heavy 3PLs are feeling the strain.

Potential causes

It is impossible to pinpoint a single, dominant cause driving the transport price reduction, and, in all likelihood, a single cause does not exist. The contraction is instead attributable to multiple, inter-related factors, each contributing a varying degree of individual influence.

During the first quarter of 2025, the economy seemed strong. A warm, late Easter then provided a further boost to trade, as companies began to move goods early in anticipation of a busy spring season. June’s transport price reduction may simply reflect a correction.

This logic aligns with ONS data reporting retail sales drops of 2.7% in May. We’re yet to see June figures, but consumers may be rebuilding rainy-day funds while interest rates remain high.

Data on direct debit failures corroborate the narrative. According to the ONS, the total monthly direct debit failure rate in May increased by 6% (compared to the same period last year). Whether voluntarily or otherwise, consumers appear to be cutting back.

Beyond the UK

It’s also important to look beyond the UK to understand Index fluctuations. Global trade policies remain unpredictable, and announcements about USA tariffs most likely brought shipments forward early this year. Tariff tirades, then, could also be partly responsible for lower haulage demand in June.

While it’s hard to understand exactly why transport prices fell in June, having the agility to react accordingly remains imperative. For 3PLs, that likely means the ability to collaborate with external carriers easily, which helps transport teams flex and contract operations quickly. TEG’s end-to-end logistics technology platform helps 3PLs unlock operational agility at pace in a continually uncertain world.

Industry Pulse

The GfK Consumer Confidence Index rose by 2 points last month, having dropped in May. The increase suggests consumer sentiment remains buoyant, despite supposed cutbacks. Whether sentiment materialises as consumption will become apparent as summer unfolds.

Elsewhere, the Bank of England chose to hold interest rates at 4.25% in June, countering widely anticipated long-term interest rate reductions. The decision was taken against a backdrop of “weak” UK economic growth, inflation running at 3.4%, and ongoing global insecurity. A balancing act if ever there was.

Following air strikes in Iran, the Strait of Hormuz remains open, preventing the huge impact its closure could have on oil supplies globally. The collapse of major UK fuel supplier Prax Group at the end of the month also caused temporary fuel shortage fears, before the UK government pledged to ensure ‘supplies are maintained’ and ‘protect our energy security’.

With the summer holiday season approaching, both the transport industry and consumers will be hoping to continue avoiding major shocks while enjoying a traditional uptick in demand.

Fuel Watch

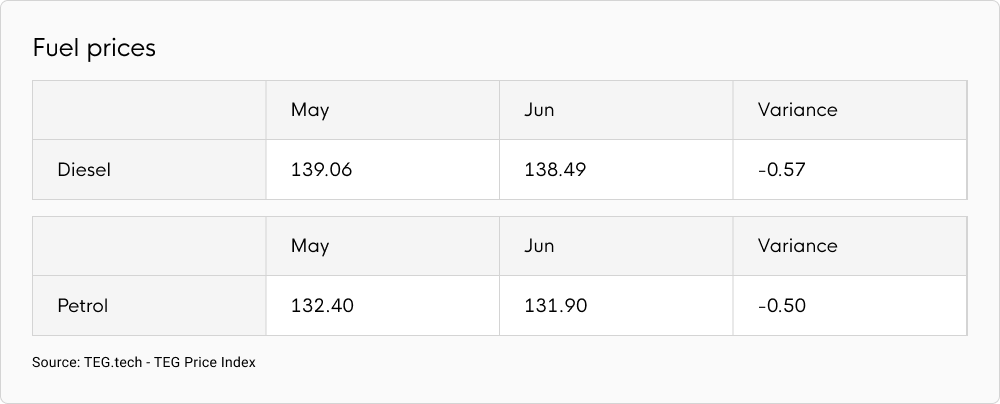

Fuel prices remained relatively stable during June, with both petrol and diesel falling only a few pence.

Diesel prices averaged 138.49p per litre in June, which was just 0.57p per litre (0.41%) lower than the previous month. Meanwhile, petrol prices averaged 131.90p per litre, falling 0.50p per litre (0.38%) compared to May’s average.

Both diesel and petrol prices remain significantly lower than they were 12 months ago, when diesel cost 8.60% more and petrol prices were 9.51% higher.

External shocks, including Iranian international relations and support for the collapsed Prax Lindsey Oil Refinery, still risk transforming the status quo.

Expert comment

“Diesel continues to be deflationary, and that is a key cost element for road transport that will be contributing to keeping TEG spot rates down. The TEG Courier Index may also be helped going forward by the Competition & Market Authority’s (CMA) report on high margins on pump prices – hauliers are much more likely to buy in bulk and so any impact in this area will have little effect on the TEG Haulier Index. Further back in the oil supply chain, the Brent Crude and WTI indices have settled back down as the risk of the Strait of Hormuz being closed seems to have subsided.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd

The TEG Price Index helps freight buyers stay ahead of change. Use it alongside our Analytics and Insights module to make strategic, data-driven logistics decisions.