Late Easter delays the surge and the market is already moving.

Index trends at a glance

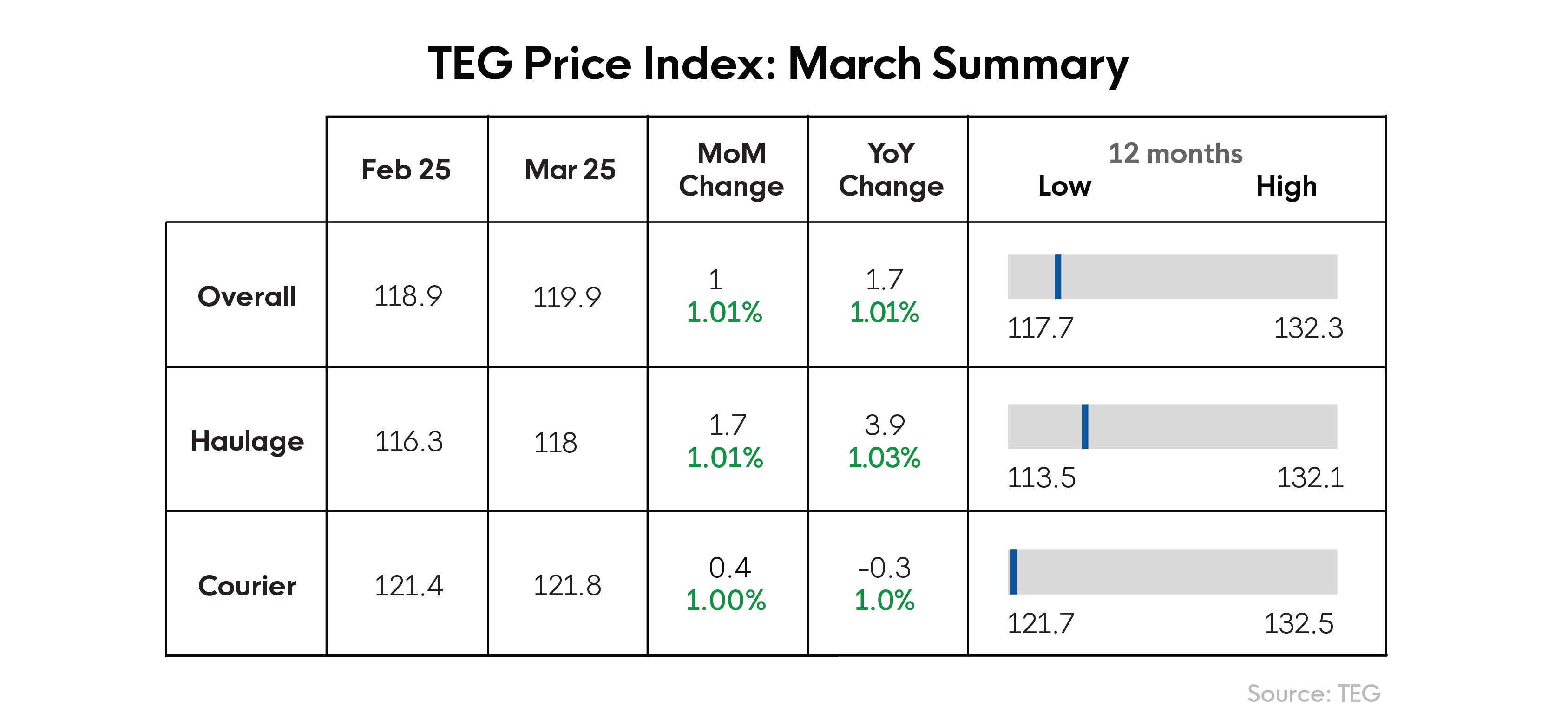

March saw the TEG Road Transport Index edge upward to 119.9, rising 1 point from February and 1.7 points year-on-year. While that’s a gentler climb than the 3.2-point jump seen last March, the story is far from quiet. There’s plenty happening behind the scenes, especially in the 13.6m Artic market, which continues to define pricing trends across the UK.

All eyes on Easter

Easter 2025 falls three weeks later than in 2024 and the effect is showing. The usual seasonal uptick in March has been delayed, with demand rising steadily but index movement held in check by strong supply.

Artics: The calm before the peak?

The artic sector is facing an unusual setup: carrier availability is up +31% vs March 2024, meaning more capacity is on the market than usual for this time of year. Yet demand is moving almost in sync with last year: up +37% month-on-month, compared to +38% in March 2024.

This creates a rare environment: easter is late, March demand is already high but additional supply is keeping price down. For freight buyers, this means an extended window to lock in competitive rates before the real pressure hits in April.

Steady haulage movement offers planning window

The haulage index rose to 118.0, up 1.7 points (1.5%) from February. That’s a solid climb, but still slightly behind historic seasonal norms. However, compared to March 2024, the index is still 2.8 points higher, a sign of ongoing cost pressures in the sector that continue to keep baseline levels elevated.

Courier conditions stable with scope for smart buying

While hauliers are gearing up for a delayed Easter rush, the courier index remained flat, nudging up just 0.4 points (0.33%) month-on-month. Interestingly, the courier index is down 0.25% year-on-year, reflecting a stabilisation of last year’s inflated levels.

“While the TEG Courier Index is still higher than its Haulier counterpart, it is Haulage that is up by 4% against last year, which was itself up 3.7% against March 2023. Meanwhile the Courier Index is similar not just to last year but is also less than 1% above March 2023. It’s probable that the movement of both indices is related to inflation - hauliers trying to catch up with previous cost rises, while anything related to consumer spending has remained more cautious until the threat of bill increases in April has been fully understood.” - Kirsten Tisdale, Logistics Expert.

What this means for freight buyers

March delivered a moment of opportunity. With availability at unusually high levels and demand rising but not yet peaking, those managing freight budgets should be making strategic decisions now.

We’ve seen early signs of demand ramping up. The shape of the Easter peak will be critical; expect a sharper climb compressed into a shorter window. For freight buyers, agility will be everything.

TEG’s end-to-end logistics technology platform matches supply and demand in real time, essential for those contracting freight in retail-driven lanes expected to spike in early April.

Industry pulse

There are signs of cautious optimism in the wider economy. The GfK Consumer Confidence Index inched up again in March, building on February’s rise, suggesting an uplift in consumer sentiment just as the retail and food sectors gear up for Easter.

At the same time, operators are feeling the cost pinch. Staffing costs are on the rise, with Adzuna data showing a 0.77% increase in average HGV salaries last month to £36,830. According to the ONS, nearly 36% of transport and logistics businesses saw increased wage costs over the last three months. With increases to the National Minimum Wage and National Insurance now in effect, those costs will climb further.

This environment demands a smart buying strategy. Freight buyers must be ready to pivot quickly, diversify contracting strategies, and use data to stay ahead of sudden cost surges or demand spikes.

The good news? Spring is here. Sunshine, Easter, and early summer activity are all expected to boost volumes. Consumers are spending, gardens are being prepped, and barbecues are getting lit.

Fuel watch

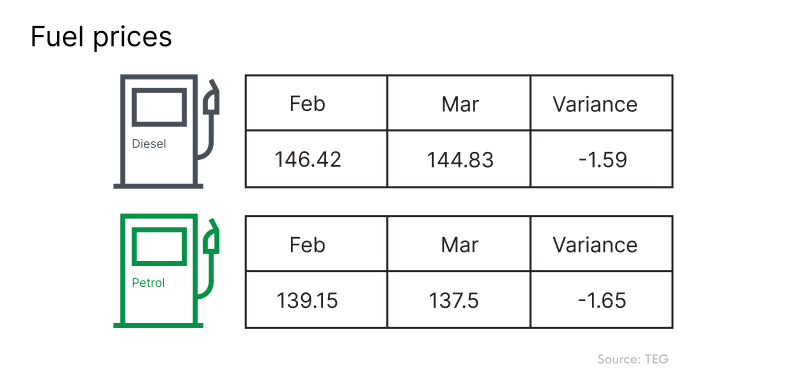

Fuel prices dipped in March, offering some relief at the pumps.

- Diesel averaged 144.83p per litre, down 1.59p (1.09%) from February, and 9.3p (6.03%) lower than this time last year.

- Petrol prices dropped to 137.5p per litre, down 1.65p (1.19%) month-on-month, and 5.04% lower year-on-year.

It’s a welcome shift after eight straight months of increases, but whether this marks the start of a new trend is still unclear.

The TEG Price Index helps freight buyers stay ahead of change. Use it alongside our Analytics and Insights module to make data-driven decisions and protect 3PLs' profitability.