TEG Index at a glance

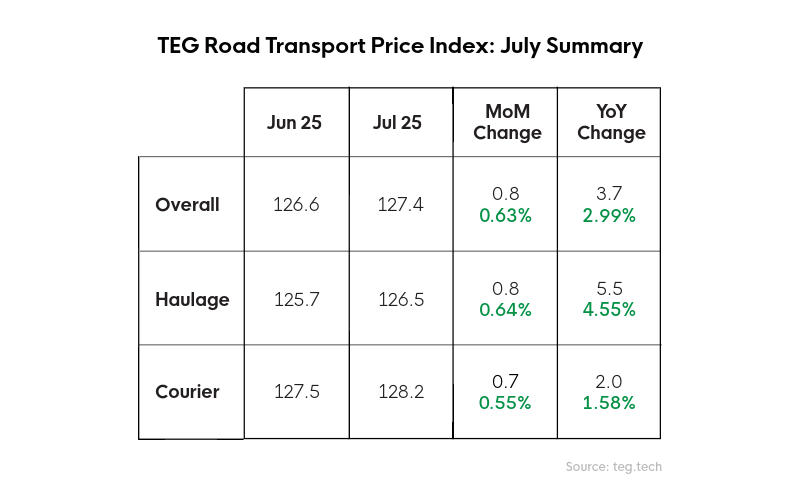

Performing off-trend for a second month, the TEG Price Index crept up by 0.8 points (0.63%) to 127.4 in July, a month that typically experiences falling prices. The July index stood 3.7 points (2.99%) higher than 12 months ago.

Following the same trend, the Haulage Price Index increased 0.8 points (0.64%) to 126.5, leaving it 5.5 points (4.55%) higher than July 2024. Interestingly, artic prices only rose 0.2 points (0.17%) in July.

The Courier Price Index rose by 0.7 points (0.55%) to 128.2, leaving it 2 points (1.58%) higher than July 2024.

July’s upward movement followed a 1.6 point (1.25%) fall in June. Both these months countered historical trends.

Supply and demand trends

Demand for artics increased by 4.94% during July, while artic supply fell by 8.40%.

Demand hikes were greater still in the market for 7.5 tonne capacity, rising by a full 13.60%. Meanwhile, the supply of 7.5 tonne capacity fell by 0.90%.

Limited vehicle availability, then, appears to be the most likely cause of price increases, and while supply and demand ultimately dictate rates, last month, several key variables shifted both.

Potential causes

July HGV driver shortages, as evidenced by vacancy figures, no doubt impacted available artic supply last month, a situation possibly compounded by employed drivers taking annual leave.

While the increase in demand for 7.5 tonne trucks may be attributable to limited HGV availability, lower grade licenced drivers still need Driver Qualification Cards (DQCs), muddying the waters. The shift in the 7.5 tonne market could therefore be attributable to the product categories in demand in July – for example, demand for furniture and white goods in summer sales.

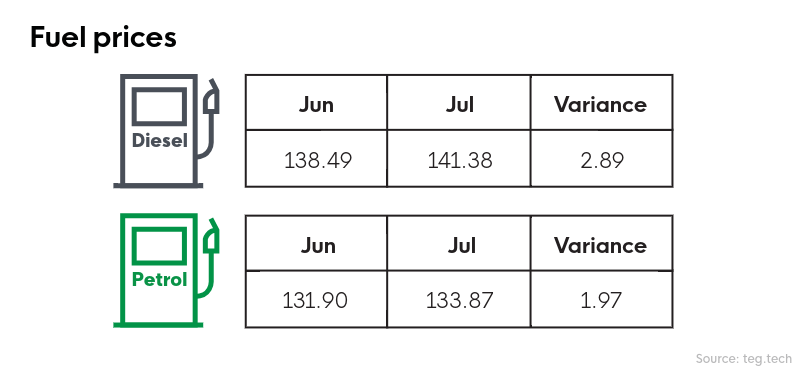

Fuel prices hardened during July for both petrol and diesel, which likely also nudged transport prices upwards.

Elsewhere, there may have been some minor market corrections in July following an unexpected transport price drop in June. Typical summer trends have proved elusive in 2025, possibly due to the introduction of fresh US tariffs first mooted in spring.

One recently reported tariff consequence relates to UK vehicle manufacturing. British car and van production in the first half of 2025 hit its lowest level since 1953 (excluding the industry shutdown during Covid). Car output fell 7.3% while van production was down 45%, with US tariff uncertainty cited as a contributing factor. The recently agreed 10% tariff on US imports from the UK came into effect on 30th June. It’s believed the clarity will stimulate production.

Industry pulse

The GkF Consumer Confidence Index fell one point in July. People appear to be developing a “wait-and-see” mindset, given speculation of tax rises in the autumn budget and inflation outstripping expectations. In June, inflation was 3.6%, up by 0.2% on May. July figures are set to be published in late August.

Interestingly, the GfK Savings Index jumped 7 points in July. This was the highest level since November 2007, suggesting those able to build up contingency funds are doing so.

Meanwhile, the International Monetary Fund (IMF) has predicted stronger global economic growth than it forecast in April, partly due to the softening of some US tariffs. The 2025 IMF global growth prediction is now 3% (and 3.1% in 2026), with the UK set to be the third fastest growing economy out of the world’s ‘advanced economies’ after the USA and Canada.

Fuel Watch

July saw diesel and petrol prices increase following a period of relative stability. Diesel prices averaged 141.38p per litre in July. This was 2.89p per litre (2.09%) higher than June. Petrol prices, meanwhile, averaged 133.87p per litre in July, rising 1.97p per litre (1.49%) on the June average price.

Despite the small rise, both diesel and petrol prices remain notably lower than in July 2024. Back then, diesel was 8.97p per litre (5.97%) higher while petrol was 10.57p per litre (7.32%) above last month’s average.

Expert comment

"GfK's saving index, which is reported separately but alongside its consumer confidence index, is 7 points higher than it was last year. And while that may be good news for building societies, it implies that consumers are being cautious about spending. Having said that, it's no surprise that the TEG Courier Index is a little up on the year, given that diesel has risen... although still deflationary against last year. On the haulage side, HGV drivers are currently in high demand meaning that the TEG Haulage Index is still rising more quickly than general inflation.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd

The TEG Price Index helps freight buyers stay ahead of change. Use it alongside our Analytics and Insights module to make strategic, data-driven logistics decisions.