TEG Index at a glance

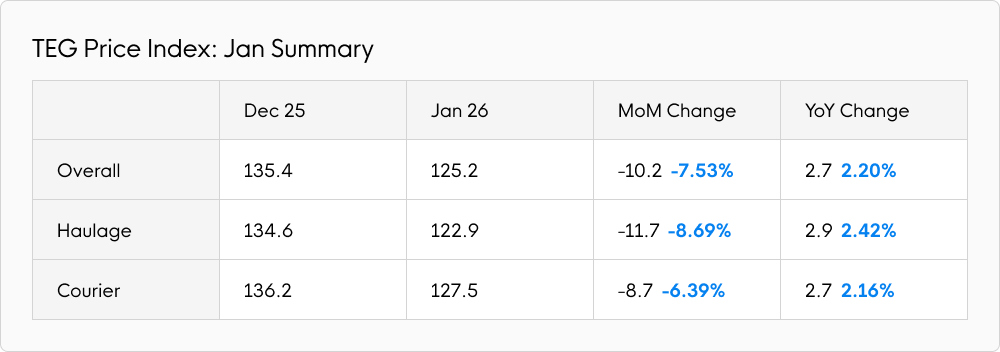

The TEG Price Index fell 10.2 points (7.53%) to 125.2 in January 2026, aligning with January 2025 movement when the index fell 9.8 points (7.4%).

Not surprisingly, the Haulage and Courier indices followed suit. Haulage fell 11.7 points (8.69%) to 122.9, while Courier dropped 8.7 points (6.39%) to 127.5. The Artic Index also fell: 12.1 points (9.6%) to reach 114.6. Again, all changes reflected 2024/2025 patterns.

Comparing year-on-year index totals, last month saw the TEG Price Index 2.7 points (2.2%) higher than in January 2025. A similar pattern was seen in Haulage, up 2.9 points (2.42%), and Courier, up 2.7 points (2.16%). The Artic Index rose 1.3 points (1.15%) year-on-year. Given annual inflation stood at 3.4% in December, it’s increasingly clear that transport prices are failing to keep pace with general price rises. That said, DHL's previously announced 4.9% annual price increase came into effect from 1 January 2026.

Demand drops following peak-season surge

Few will be surprised to learn that demand for transportation fell significantly in January. Overall, demand dropped by 18.7%. Looking specifically at Haulage, the month-on-month fall was slightly higher: 24.4%.

Meanwhile, availability surged. Again, this is something typically seen in January, following peak season. Overall, availability increased 52.4%. For Haulage, the rise was 62.0%. While such figures seem dramatic, they are as expected for January transport activity.

“Resilient” consumer confidence

When considering sentiment on spending and broader economic health, shifts in the GfK Consumer Confidence Index remain a reliable indicator. January 2026 saw the Index rise one point, compared to January 2025, when it dropped 5 points. The bump means consumer confidence is net positive for the first time in ten years, with consumers apparently more confident about managing their personal finances but unsure about the wider economic outlook. According to Neil Bellamy, Consumer Insights Director at GfK, the message is one of “resilience” rather than optimism.

Elsewhere, business confidence also started the year positively. The ONS Business Insights and Conditions Survey stated that, in the two weeks ending 18 January 2026, 20.2% of respondents thought their business’s performance would increase over the next 12 months, while only 15.0% thought it would decrease.

Industry pulse

While inflation rose to 3.4% in December, the hike was largely due to anomalous factors such as higher aviation prices over the festive period and higher tobacco prices following increased taxation.

Interest rates, at 3.75%, will be reviewed on 5 February. Many expect a gradual fall this year, but few expect a cut this week.

The average HGV driver salary dropped by 3.34% to £41,403 in January, reflecting much lower demand for the movement of goods. HGV driver salaries now sit below the national average salary (£42,309) for the first time since June 2025. HGV vacancies also continued to fall in January.

Geopolitical events dominated headlines last month, with American hostility towards Greenland and instability in Iran both unsettling economic sentiment. Fortunately, at the time of writing, both situations have eased. Better still, major oil producers have since agreed to keep output unchanged, probably influencing fuel prices (see below).

Closer to home, the UK government’s recent negotiations with China should help to make UK exports to China easier, with the Prime Minister welcoming new export deals totalling over £400 million. This activity should lead to a boost in transportation demand during 2026.

Fuel Watch

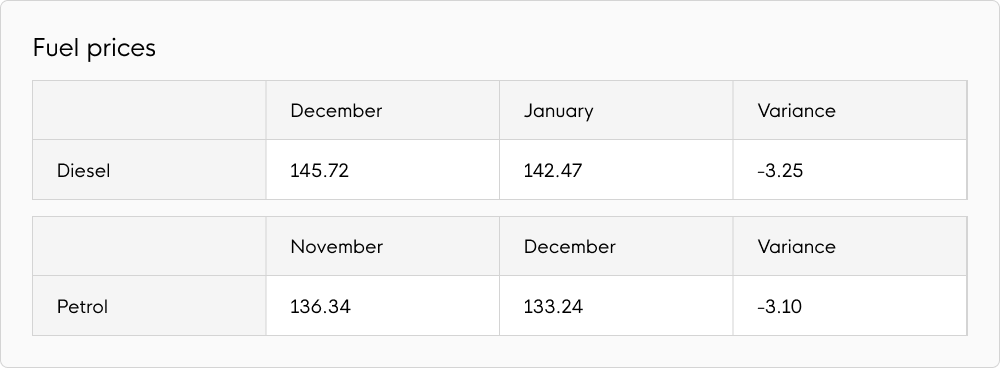

In a positive start to 2026, the price of petrol dropped to its lowest level since the summer of 2021, according to RAC Fuel Watch. Diesel prices saw a notable fall in January, too.

Average petrol prices fell 3.1p (2.27%) to 133.24p per litre. Year-on-year, this was a substantial 4.2p per litre (3.06%) reduction. The RAC suggests the fall was driven by oil dipping below the $60 a barrel mark on 7 January – the first time it has done so since February 2021.

Diesel price falls weren’t far behind in January. Following a 3.25p (2.23%) drop, the average price was 142.47p per litre. That was 1.65p per litre (1.14%) lower than in January 2025.

This good news will be welcomed by transport operators and consumers filling up at the pumps, helping to bolster New Year optimism.

Expert comment

“At this time of year hauliers have to hope that their customers value service over cost and future sustainability over margin. As every year, the seasonal peak and consequent squeeze on resources that is Black Friday and Christmas is past. As every year, spot rates for road transport have dropped and the salaries for drivers in job ads have done the same. Although the talk in corporate boardrooms will be about the environment and decarbonisation being priority, in the yard the focus at this time of year is a very different one: managing resources tightly enough to achieve the efficiency to survive.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd

TEG technology helps 3PLs run more efficiently. More detailed information is available via our Carrier Sourcing module.