TEG Index at a glance

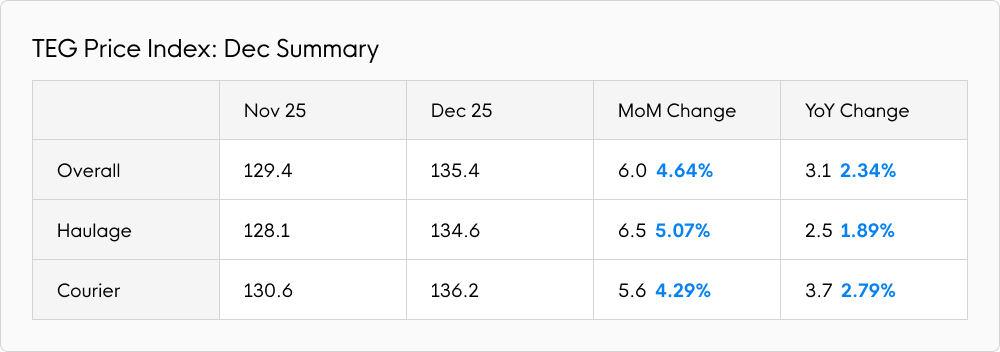

The TEG Price Index rose 6 points (4.64%) in December to reach 135.4 – the highest ever level for the overall Index.

Marked increases were also evident for the Haulage and Courier Index subcomponents (although neither the Haulage nor the Courier Index achieved a standalone record high).

Haulage prices rose by 6.5 points (5.07%) to 134.6 while courier prices increased by 5.6 points (4.29%) to reach 136.2. Meanwhile, the Artic Index rose 7.2 points (6.0%) in December to reach 126.7.

Year-on-year, the overall TEG Index has risen by 3.1 points (2.34%). While the Courier Index has kept pace, rising 3.7 points (2.79%), the Haulage Index lagged behind. It rose by just 2.5 points (1.89%) in the past 12 months.

Annual price jump trails inflation

TEG data suggests the increase in 2025 transport prices failed to match annual inflation. Compared to the 3.2% annual Consumer Price Index (CPI) growth rate reported on 17 December, the overall TEG Index rose by 2.34% in 2025 and the Haulage Index by just 1.89%.

Price increases were even more muted for the Artic Index. It rose by 1.12% in 2025 – less than half the annual rate of inflation.

To call 2025 challenging would be no surprise to any logistics operator. According to Adzuna, average HGV salaries rose 8.50% from January to December 2025, and government statistics show diesel prices have risen by 2.18%. That’s in addition to economic changes impacting operating costs, such as employers’ National Insurance increases as of April 2025.

And yet, overall, the logistics industry stood firm, with many operators pioneering new efficiency strategies to bolster under-pressure margins. With 2026 bound to usher in further challenges, efficiency will remain the centrepiece of many a corporate agenda.

Availability shrinks by 22.89%

With the Christmas surge in full swing last month, it was perhaps unsurprising to see carrier availability nosedive by 22.89%, triggering customary December price hikes. While it’s too early to establish a clear picture of retail performance over the 2025 festive period, several statistics of interest have already surfaced.

According to MRI Software, December footfall was 3.9% higher than last year, suggesting a “resilient” performance for retailers. BDO’s High Street sales tracker showed that total like-for-like sales rose 1.0% in the week ending 21 December, reversing two consecutive weeks of decline. However, the increase came against 2.6% growth in the same week last year, highlighting fragility in consumer demand.

Meanwhile, the British Retail Consortium (BRC) reported that shoppers spent more in December (3.2%) compared with the year before, but this wasn't enough to make up for an overall lacklustre year for retailers. It also highlighted that many Black Friday sales fell into December when they’re normally contained in November figures. On a positive note, a two-point increase in the GfK Consumer Confidence Index suggests December spirits remained buoyant.

Industry pulse

Both interest rates and inflation dropped in December. The Bank of England’s Monetary Policy Committee (MPC) voted to cut interest rates by 0.25% to 3.75% on 18 December. Further reductions are widely expected during 2026.

CPI inflation fell to 3.2%, down from 3.6% in October. In comparison, Eurozone inflation was 2.1% in November 2025.

Elsewhere, average HGV driver salaries fell by £122 to £42,838 in December, following monthly increases since February 2025 (aside from an £8 drop in November). It’s too soon to tell whether this is a momentary blip or the start of HGV salaries levelling out.

BBC Insights Unit and the British Chamber of Commerce completed a survey of 4,600 businesses in December. 91% of those interviewed were small to medium-sized enterprises (SMEs). While the results suggested a fall in business confidence during Q4, they did find that 46% were expecting increased turnover in the next 12 months (48% in Q3). The survey also indicated 52% of firms are looking to raise prices in the next three months (44% in Q3). Pressure on costs is evident across all sectors.

Internationally, all eyes will be on the political tumult of Venezuela. According to the US Energy Information Administration, the country holds about 17% of global crude oil reserves, which means its geopolitical stability has the potential to sway global oil prices. Oil production in the country has been limited of late. With all else equal, an increase in production will reduce oil prices.

Fuel Watch

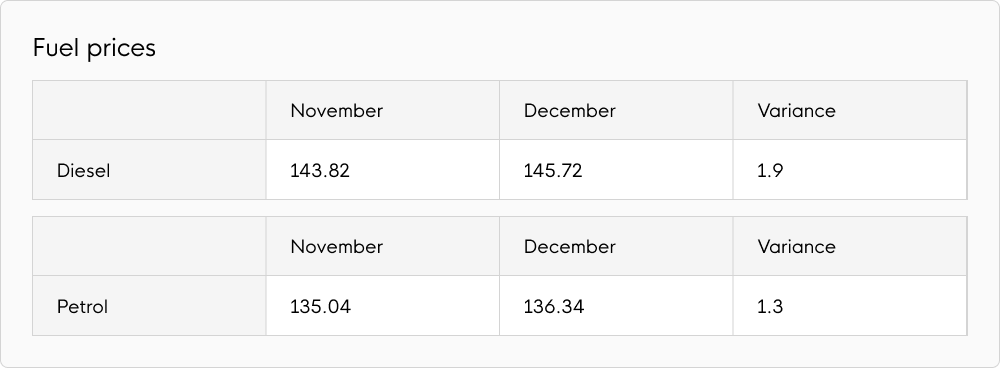

Both diesel and petrol prices rose during December. Average diesel prices rose by 1.9p per litre (1.32%) to 145.72p, while average petrol prices rose by 1.30p per litre (0.96%) to 136.34p.

Year-on-year, fuel costs were also up. Diesel prices rose 3.11p per litre (2.18%), while petrol prices experienced a more muted lift of 0.06p per litre (0.04%).

Elsewhere, the UK government has now released details of the fuel duty taper that will start from 1 September 2026. The reversal of the 5p duty cut will take place in three stages: 1p on 1 September, 2p on 1 December, and 2p on 1 March 2027. This will return rates to pre-March 2022 levels. Finally, the planned 2026-27 inflation increase will not take place. Instead, the government will uprate fuel duty rates by the Retail Price Index (RPI) from April 2027.

Expert comment

“As we enter the new year, 2025 will probably be remembered for Trump and tariffs; the various cyber-attacks - think M&S, Co-op, Harrods and particularly JLR; and that late budget having a dampening effect on the economy. Given that, it’s perhaps no surprise that both the TEG Haulage and Courier indices showed quite restrained year-on-year inflation in December and stopped just short of their previous December highs in 2021 and 2022 respectively.”

Kirsten Tisdale – Senior Logistics and Supply Chain Consultant – Aricia Ltd

The TEG Price Index helps freight buyers stay ahead of change. More detailed pricing statistics are available via our Analytics and Insights module.